Multi-Million-Dollar Financial Fraud

Ponzi Scheme Ends in Prison Time for Former Pro Football Player and Bank Executive

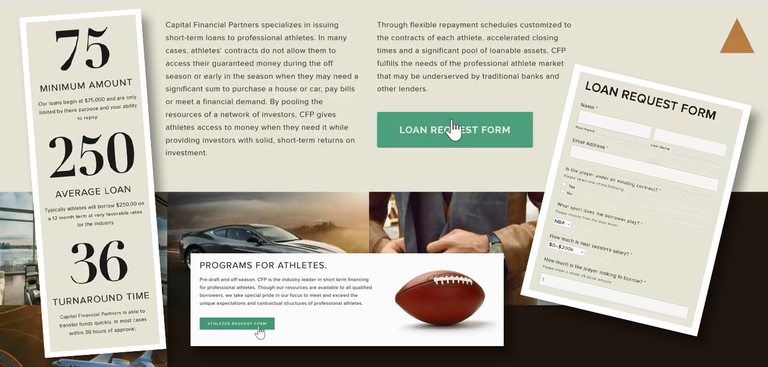

Former NFL player Will Allen and former bank executive Susan Daub’s company website, parts of which are shown, appeared legitimate and hid from investors the fact that it was being used to run a Ponzi scheme.

The financial pitch was compelling—help fund short-term loans to professional athletes and get a high interest rate return on your investment, perhaps as high as 18 percent. Equally as compelling were the pitchmen: businessman Will Allen was a former pro football standout who played for the New York Giants and Miami Dolphins; his business partner, Susan Daub, was a former bank executive.

Allen and Daub’s Massachusetts company, Capital Financial Partners (CFP), operated out of Florida and took in more than $35 million in approximately three years. But in return for their money, many investors got back headaches, because Allen and Daub were running a Ponzi scheme.

“The company made some legitimate loans,” said Special Agent Sheila Magoon, a financial fraud expert who investigated the case out of the FBI’s Boston Division, “but relatively early on, they began to defraud investors. Allen and Daub surely knew what they were doing was criminal.”

While it might seem surprising that highly paid professional athletes need loans, there are circumstances where that is indeed the case. An athlete just out of college, for example, can sign a lucrative professional contract but might not be paid until he starts playing. A short-term loan would bridge the gap until he gets a regular paycheck.

“Let’s say Athlete A wanted a loan of $1 million,” Magoon explained. “CFP went looking for specific investors to loan money to Athlete A. That gave investors even more enthusiasm, knowing they were helping a particular player.”

Although there was no standard loan amount, Magoon said, investors typically put up at least $100,000. Between 2012 and April 2015, Allen, 38, and Daub, 56, defrauded dozens of investors and diverted some of the funds for their personal use.

Sometimes the pair collected investor money to fund nonexistent loans and used the money to pay themselves and invest in other unrelated businesses. Other times, they told investors that the athlete loans were larger than they actually were, allowing Allen and Daub to collect more money than they were lending.

To keep investors from discovering the fraud, the pair also used newly invested money to make payments to existing investors.

“We researched what they claimed their business was—what they said they were doing and what they were actually doing,” Magoon said. Working with the Internal Revenue Service Criminal Investigation Division, the investigators conducted interviews and analyzed financial and other records. At the same time, the Securities and Exchange Commission (SEC) was conducting a civil investigation.

In June 2015, Allen and Daub were arrested on criminal charges after being sued by the SEC. In November 2016, each pleaded guilty to wire fraud, conspiracy, and money laundering. Of the more than $35 million Allen and Daub received in investments, less than $22 million has been repaid to date.

This past March, a federal judge in Boston sentenced Allen and Daub to six years in prison and three years of supervised release; they were also ordered to pay restitution of approximately $16.8 million. The judge called Allen and Daub’s crimes an “outrageous, extensive fraud.”

“Relatively early on, they began to defraud investors. Allen and Daub surely knew what they were doing was criminal.”

Sheila Magoon, special agent, FBI Boston